Silicon Carbide Market Analysis and Insights:

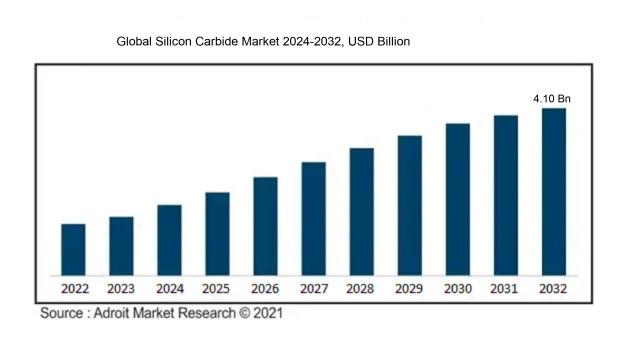

The silicon carbide market was estimated to be worth USD 2.32 billion in 2023. According to projections, the silicon carbide market would expand at a compound annual growth rate (CAGR) of 6.65% from 2024 to 2032, from USD 3.98 billion to USD 4.10 billion.

The Silicon Carbide (SiC) Market is largely influenced by the growing need for energy-efficient power electronics. SiC is favored for its excellent thermal conductivity and its ability to withstand high electric field strengths, making it ideal for applications in electric vehicles (EVs), renewable energy installations, and industrial power supply systems. The worldwide movement towards sustainable energy is accelerating the use of SiC components, which enhance the efficiency of power conversion and management processes. Additionally, the expansion of the automotive sector, particularly with the increasing prevalence of electric and hybrid vehicles, is a significant factor in the growth of the SiC market, due to its performance at elevated temperatures and voltages. Furthermore, improvements in manufacturing processes are leading to reduced costs for SiC substrates, complemented by rising investments in research and development initiatives that are driving market growth. As various industries increasingly shift towards environmentally friendly solutions, the demand for high-performance semiconductor materials like Silicon Carbide is expected to persist, solidifying its essential role in future technological developments.

Silicon Carbide Market Definition

Silicon carbide, a compound semiconductor formed from the combination of silicon and carbon, is renowned for its remarkable hardness and superior thermal conductivity. This material finds extensive application in advanced electronic devices, abrasive products, and environments that require high-temperature durability.

Silicon carbide (SiC) is an essential semiconductor that is celebrated for its remarkable electrical characteristics, excellent thermal conductivity, and high-temperature endurance, positioning it as an optimal choice for power electronics and high-frequency applications. Its capability to function effectively at increased voltages and temperatures significantly enhances the efficiency of energy systems, especially in the domains of renewable energy and electric vehicles. SiC components contribute to reduced energy losses, thus boosting overall performance and reliability across various uses, such as electric motors and inverters. Furthermore, its resilience and strong mechanical attributes make it suitable for challenging environments, facilitating progress in telecommunications, aerospace, and industrial sectors.

Silicon Carbide Market Segmental Analysis:

Insights On Key Product

Green

The Green type of silicon carbide is expected to dominate the Global Silicon Carbide Market due to its superior properties and increasing demand in high-performance applications. The Green product is characterized by its high purity and semiconductor quality, making it ideal for use in electronics, power devices, and LED applications. With the escalating need for energy-efficient and high-performance materials, especially in automobile and electronics sectors, the growth in electric vehicles (EVs) further drives the demand for Green silicon carbide. Furthermore, its usage in renewable energy systems and advanced manufacturing processes positions it favorably in the market.

Black

Black silicon carbide, known for its significant hardness and low thermal expansion, is widely utilized in abrasive applications, such as sandblasting, grinding, and cutting. This variant is less expensive than the Green type and has established a solid demand in industries such as metalworking and construction. However, while its market presence is substantial, especially for cost-sensitive applications, it does not match the burgeoning requirements for high-performance, high-purity applications that Green silicon carbide caters to, making it less of a growth driver in the current landscape.

Others

The 'Others' category includes various specialized forms of silicon carbide, such as alpha or beta silicon carbide, which are utilized in niche applications tailored to specific needs. Although this may hold some potential for growth in specific sectors like ceramics and specialty abrasives, its overall share in the market is comparatively minor. Its limited applicability restricts its dominance, particularly when juxtaposed against the robust growth seen in the Green and Black categories. Thus, while it offers certain benefits, it lacks the broader appeal and market traction of the more prominent types.

Insights On Key Device

Discrete Devices

Discrete Devices are expected to dominate the Global Silicon Carbide Market due to their extensive application in power electronics and high-temperature environments. These devices are favored for their efficiency in energy conversion, which is increasingly important in sectors such as automotive (especially electric vehicles), renewable energy, and industrial equipment. The growing demand for energy-efficient solutions, coupled with advancements in the technology surrounding SiC-based discrete devices, is driving this trend. Additionally, their ability to handle high voltages and temperatures makes them an ideal choice for modern power management systems, resulting in superior performance compared to traditional silicon devices.

Bare Die

Bare Die represent a smaller yet notable portion of the Global Silicon Carbide Market. While they lack the form factor of discrete devices, Bare Die are increasingly utilized in specialized applications requiring custom solutions. The flexibility to integrate Bare Die into system-on-chip (SoC) architectures allows for higher efficiency and greater power density. This can be advantageous in applications where space is at a premium, such as in aerospace and defense technologies. The rise in custom semiconductor solutions is likely to continue influencing the adoption of Bare Die in specific niche markets, even if they don't dominate the overall market.

Insights On Key End-User

Automotive

The automotive sector is anticipated to dominate the Global Silicon Carbide Market primarily due to the increasing demand for electric vehicles (EVs) and hybrid vehicles. Silicon carbide is extensively utilized in power electronics, enabling efficient energy conversion and management within EVs. With the automotive industry shifting towards these advanced technologies to enhance performance and reduce emissions, the adoption of silicon carbide components is expected to surge. Additionally, the need for faster charging solutions and improvements in electric motor efficiency further solidify its position in this sector, making automotive the leading application for silicon carbide technologies.

Steel

The steel industry is a significant consumer of silicon carbide due to its application in the steel manufacturing process. Silicon carbide enhances the efficiency of metallurgical processes, acting as a deoxidizing agent, which improves the quality of the steel produced. The continuing demand for steel in construction and manufacturing industries drives the growth of this market, offering a robust framework for the use of silicon carbide. Furthermore, the push for higher-grade steel products will likely lead to increased consumption of silicon carbide over time.

Aerospace

The aerospace sector represents a niche but important area where silicon carbide is increasingly valued for its lightweight and heat-resistant properties. Components made from silicon carbide are used in various aerospace applications, such as turbine engines and airframe structures, where performance and durability are crucial. The ongoing advancements in aerospace technology and the continuous need for improved fuel efficiency further promote the integration of this material. As aviation and space exploration expand, the relevance of silicon carbide in this field is expected to grow, albeit at a slower pace than automotive.

Defence and Military

In the defence and military sectors, silicon carbide is recognized for its applications in protective equipment and electronic systems. The compound's properties support the creation of lightweight, durable materials that are essential for military applications where reliability in extreme conditions is necessary. However, the growth in this area is largely driven by government budgets and initiatives, making it variable compared to other industries. While the importance of silicon carbide persists, its market share in the overall landscape remains limited relative to automotive and aerospace.

Healthcare

The healthcare sector utilizes silicon carbide primarily for medical devices and equipment due to its biocompatibility and sterilization capabilities. While growth in this domain is steady, it is hampered by regulatory constraints and slower adoption rates in comparison to more lucrative markets like automotive. Innovations in medical technology do present opportunities for silicon carbide; however, its overall usage remains less prevalent when compared to industries with immediate and substantial demand for high-performance material applications.

Electrical and Electronics

The electrical and electronics industry is witnessing steady growth in the application of silicon carbide for semiconductor devices and power electronics. Silicon carbide components provide advantages like higher efficiency and thermal stability, which are essential for modern electronic applications. However, competition from other semiconductor materials and potential market saturation restrict the growth potential in this sector. Thus, while silicon carbide plays a role in transitioning to more efficient electronic systems, it does not dominate this space as strongly as automotive does.

Global Silicon Carbide Market Regional Insights:

Asia Pacific

The Asia Pacific region is projected to dominate the global silicon carbide market due to its rapid industrialization, increasing investments in electric vehicle (EV) manufacturing, and the rising demand for advanced semiconductor materials. Countries like China, Japan, and South Korea are at the forefront of technological advancement and production capabilities, making substantial contributions to silicon carbide innovations. Furthermore, the growing renewable energy sector in this region enhances the adoption of semiconductor devices, further positioning Asia Pacific as the leader in silicon carbide utilization. The region's strategic government policies promoting electric mobility and energy efficiency further emphasize its dominance in this market.

North America

North America, particularly the United States, is a significant player in the silicon carbide market, primarily driven by the automotive sector's shift towards electric vehicles and robust semiconductor manufacturing capabilities. The presence of key industry players and ongoing R&D investments bolster market growth. Additionally, the increased focus on renewable energy and power electronics applications continues to augment demand for silicon carbide technologies, making it a vital region in the silicon carbide landscape.

Europe

Europe is witnessing a surge in silicon carbide demand fueled by the EU's commitment to sustainability and reducing carbon emissions. The automotive industry, especially in Germany and France, is driving the adoption of silicon carbide in electric vehicles and other energy-efficient technologies. Moreover, the region is focusing on developing a circular economy, which further entails innovation and investment in semiconductor technologies, maintaining Europe's relevance in the global silicon carbide market.

Latin America

In Latin America, the silicon carbide market is gradually expanding, although it is not as dominant as other regions. The growth is primarily attributed to the increasing awareness and adoption of renewable energy sources, which create demand for semiconductor applications. Countries like Brazil and Mexico are beginning to invest in silicon carbide technologies, but this region remains largely underrepresented in comparison to its counterparts, with growth potential depending on more robust industrial policies and technology transfer.

Middle East & Africa

The Middle East and Africa region presents a growing but smaller share of the global silicon carbide market. The rise in renewable energy projects and a focus on technological advancements in electrical systems drive interest in silicon carbide. However, the region's market remains limited due to challenging economic conditions and underdeveloped infrastructure. For growth to be realized, increased collaboration with global firms and investment in local manufacturing capabilities will be essential to harness the potential of silicon carbide technologies.

Silicon Carbide Competitive Landscape:

Major contributors in the global Silicon Carbide industry propel innovation by focusing on the advancement of materials and forming strategic alliances, with the goal of improving energy efficiency in a range of applications. Their partnerships with sectors like automotive and electronics facilitate the broader integration of silicon carbide technologies.

Prominent entities in the Silicon Carbide sector comprise Cree, Inc. (currently known as Wolfspeed), ROHM Co., Ltd., STMicroelectronics N.V., ON Semiconductor Corporation, Infineon Technologies AG, Mitsubishi Electric Corporation, Nexperia B.V., II-VI Incorporated, Asahi Kasei Corporation, and Silicon Carbide Technology, Inc. Furthermore, firms like Qorvo, Inc., EpiGaN, GeneSiC Semiconductor, and General Electric Company play crucial roles in this market. Additional noteworthy participants include Norstel, Inc., Semikron International GmbH, and Texas Instruments Incorporated. These organizations are actively involved in the innovation, production, and commercialization of Silicon Carbide technologies for a variety of applications.

Global Silicon Carbide COVID-19 Impact and Market Status:

The Covid-19 pandemic significantly affected the Global Silicon Carbide market by interrupting supply chains and hindering production rates, all the while driving up demand in industries such as semiconductors and electric vehicles.

The COVID-19 pandemic had a profound impact on the Silicon Carbide (SiC) market, presenting both hurdles and opportunities in multiple industries. Initially, supply chain disruptions impeded the production and distribution of SiC components, resulting in delays that particularly affected the automotive and electronics sectors, which are vital for electric vehicles and power devices. Nonetheless, the recovery phase saw a notable pivot towards green technologies and renewable energy, underscoring the critical role of SiC in boosting energy efficiency and enhancing performance in semiconductor applications. The surge in electric vehicle demand, fueled by government incentives and changing consumer preferences, further accelerated the growth of the SiC market. Moreover, the pandemic highlighted the semiconductor sector's robustness, which has set the stage for significant advancements in SiC technology. As economies begin to stabilize, the market is expected to witness considerable growth, bolstered by continuous investments in energy-efficient technologies and a rebound in demand across various end-user sectors.

Latest Trends and Innovation in The Global Silicon Carbide Market:

- In April 2021, ON Semiconductor announced the acquisition of the SiC business from the German company, GaN Systems, strengthening its position in the power semiconductor market with advanced SiC technology.

- In August 2021, Wolfspeed, a subsidiary of Cree, unveiled its new 200 mm Silicon Carbide manufacturing facility in Durham, North Carolina, significantly increasing its production capacity to meet the growing demand for electric vehicles and renewable energy applications.

- In September 2022, Infineon Technologies completed the acquisition of Cypress Semiconductor's silicon carbide business, enhancing Infineon's portfolio with advanced power semiconductor technologies tailored for automotive and industrial applications.

- In October 2022, STMicroelectronics announced a partnership with GaN Systems to co-develop advanced power solutions that leverage both SiC and GaN technologies, aimed at delivering higher efficiency and performance in power conversion applications.

- In January 2023, Mitsubishi Electric Corporation expanded its SiC product lineup by introducing new SiC power devices aimed at the automotive , targeting improved performance and energy efficiency in electric vehicles.

- In March 2023, Texas Instruments launched a new series of SiC MOSFETs, emphasizing their lower conduction losses and higher efficiency, addressing the needs for automotive and industrial applications.

- In June 2023, the semiconductor company, Semikron, announced an expansion of its production capabilities in Germany, focusing on SiC modules for the growing electric vehicle market, positioning itself as a key player in sustainable energy solutions.

- In August 2023, ROHM Semiconductor announced the establishment of a dedicated research and development center for Silicon Carbide technology in Japan, aimed at accelerating innovation and commercialization of SiC power devices.

- In September 2023, GlobalFoundries and Qorvo formed a strategic partnership to enhance their silicon carbide processing techniques, focusing on optimizing the performance of RF (radio frequency) devices for telecommunications and automotive applications.

Silicon Carbide Market Growth Factors:

The expansion of the Silicon Carbide market is propelled by a rising need for energy-efficient solutions and advanced semiconductor functionalities in multiple sectors.

The Silicon Carbide (SiC) market is currently witnessing remarkable expansion, spurred by a variety of influential factors. Primarily, the rising need for energy-efficient technologies in the power electronics industry is driving the adoption of SiC, attributed to its exceptional thermal conductivity and high electric field strength, which optimize performance under elevated temperatures and voltages. Additionally, as electric vehicle (EV) usage becomes more widespread, there is an increasing requirement for advanced semiconductor materials that enhance battery management systems and power inverters, making SiC a favored option among manufacturers.

The growth of renewable energy sources, including solar and wind, further amplifies the demand for SiC devices, crucial for effective energy conversion and management. Moreover, the global emphasis on minimizing carbon emissions is motivating industries to transition to SiC technology, given its reduced environmental impact compared to conventional silicon alternatives. Innovations driven by new applications in sectors such as aerospace, telecommunications, and healthcare continue to promote investment and development in SiC technologies.

Furthermore, strategic partnerships and advancements in production techniques are improving the accessibility and cost-effectiveness of SiC components, thereby accommodating a broader spectrum of applications and fueling market growth. Altogether, these elements illustrate a promising outlook for the Silicon Carbide market in the forthcoming years, offering a wealth of opportunities across diverse industries.

Silicon Carbide Market Restaining Factors:

The primary challenges facing the Silicon Carbide market are the elevated manufacturing expenses and the restricted access to essential raw materials.

The Silicon Carbide (SiC) sector is confronted with numerous obstacles that could impede its growth trajectory. A primary concern is the elevated production costs linked to SiC materials and components, which may discourage manufacturers from moving away from conventional silicon technologies. In addition, the scarcity of high-quality SiC substrates presents challenges for scaling production across various sectors, including power electronics and semiconductor manufacturing. The intricate nature of SiC processing and the requirement for specialized fabrication methods may further complicate entry into the market for new entrants. Additionally, there is stiff competition from established materials like silicon, as well as from newer alternatives such as gallium nitride (GaN), which could hinder SiC's uptake in specific markets. Furthermore, global economic volatility and supply chain challenges, exacerbated by the COVID-19 pandemic, add to the uncertainties within the market. Nevertheless, the increasing demand for energy-efficient and high-performance electronic solutions presents significant opportunities for innovation and progress in the SiC arena, as industries place a greater emphasis on sustainability and the integration of advanced technologies.

Key Segments of the Silicon Carbide Market

By Product

- Black

- Green

- Others

By Device

- Discrete Devices

- Bare Die

By End-User

- Steel

- Automotive

- Aerospace

- Defence and Military

- Healthcare

- Electrical and Electronics

- Others

Regional Overview

North America

- US

- Canada

- Mexico

Europe

- Germany

- France

- U.K

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- Rest of Asia Pacific

Middle East and Africa

- Saudi Arabia

- UAE

- Rest of Middle East and Africa

Latin America

- Brazil

- Argentina

- Rest of Latin America